WebMail

WebMail  LiveChat

LiveChat Allowance for Doubtful Accounts Journal Entry + Example

Content

- What is a bad debt expense?

- Uncollectible Accounts Receivable FAQs

- Allowance Method: Journal Entries (Debit and Credit)

- Contra Equity Account

- Balance Sheet Aging of Receivables Method for Calculating Bad Debt Expenses

- Pareto Analysis Method

- What Happens to the Balance Sheet When Accounts Receivable Is Collected?

Including contra accounts on a balance sheet is important as it allows for a more transparent view of a company’s financial position. This is done by separating the decreases that have occurred in the contra account from the original transaction amount. This allows the reader to see both the current and historical book values for a particular asset or liability.

- This is done by separating the decreases that have occurred in the contra account from the original transaction amount.

- The subsidiary ledger allows the company to access individual account balances so that appropriate action can be taken if specific receivables grow too large or become overdue.

- For example, if 3% of your sales were uncollectible, set aside 3% of your sales in your ADA account.

- With this method, accounts receivable is organized into categories by length of time outstanding, and an uncollectible percentage is assigned to each category.

- In the event that a contra account is not utilized, it can become increasingly troublesome to determine historical costs, which makes tax preparation time-consuming and difficult.

This is done to entice customers to keep products instead of returning them. GAAP since the expense is recognized in a different period as when the revenue was earned. Estimates are inherent in accounting because the accountant attempts to match revenues and expenses. During the year, similar entries are made to record other accounts declared uncollectible. However, some firms show this item as a deduction from gross sales in arriving at net sales.

What is a bad debt expense?

See the encyclopedia entry Balance sheet for more explanation of the above statement. For working examples of interrelated financial statements and coverage of financial statement metrics, see Financial Metrics Pro. Writing off the debt this way, incidentally, does not relieve the debtor of the obligation to pay. The seller undertakes the write off in the interest of accounting accuracy, but the customer is still liable for the debt. The seller retains every right to pursue payment by other legal means, such as engaging a collection service or filing a lawsuit.

The allowance for doubtful accounts (or the “bad debt” reserve) appears on the balance sheet to anticipate credit sales where the customer cannot fulfill their payment obligations. Using the example above, let’s say that a company reports an accounts receivable debit balance of $1,000,000 on June 30. The company anticipates that some customers will not be able to pay the full amount and estimates that $50,000 will not be converted to cash. Additionally, the allowance for doubtful accounts in June starts with a balance of zero.

Uncollectible Accounts Receivable FAQs

It may be obvious intuitively, but, by definition, a cash sale cannot become a bad debt, assuming that the cash payment did not entail counterfeit currency. Allowance for uncollectible accounts is a contra asset account on the balance sheet representing accounts receivable the company does not expect to collect. https://www.bookstime.com/ When customers buy products on credit and then don’t pay their bills, the selling company must write-off the unpaid bill as uncollectible. Allowance for uncollectible accounts is also referred to as allowance for doubtful accounts, and may be expensed as bad debt expense or uncollectible accounts expense.

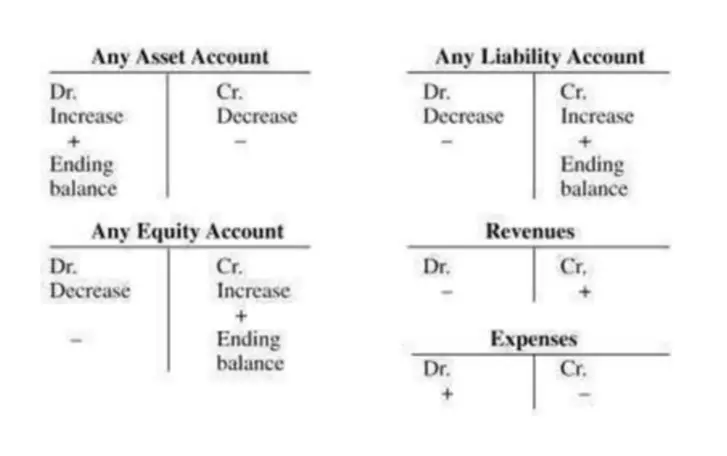

So for an allowance for doubtful accounts journal entry, credit entries increase the amount in this account and debits decrease the amount in this account. The allowance for doubtful accounts account is listed on the asset side of the balance sheet, but it has a normal credit balance because it is a contra asset account, not a normal asset account. For more ways to add value to your company, download your free A/R Checklist to see how simple changes in your A/R process can free up a significant amount of cash. [box]Strategic CFO Lab Member Extra

Access your Cash Flow Tune-Up Tool Execution Plan in SCFO Lab. The journal entry for the Bad Debt Expense increases (debit) the expense’s balance, and the Allowance for Doubtful Accounts increases (credit) the balance in the Allowance. The allowance for doubtful accounts is a contra asset account and is subtracted from Accounts Receivable to determine the Net Realizable Value of the Accounts Receivable account on the balance sheet.

Allowance Method: Journal Entries (Debit and Credit)

For example, a company has $70,000 of accounts receivable less than 30 days outstanding and $30,000 of accounts receivable more than 30 days outstanding. Based on previous experience, 1% of accounts receivable less than 30 days old will be uncollectible, and 4% of those accounts receivable at least 30 days old will be uncollectible. Two primary methods exist for estimating the dollar amount of accounts receivables not expected to be collected. If a doubtful debt turns into a bad debt, credit your Accounts Receivable account, decreasing the amount of money owed to your business. For example, if 3% of your sales were uncollectible, set aside 3% of your sales in your ADA account.

Is the allowance for doubtful accounts a contra asset account that equals multiple choice question?

Answer choice: a.

The allowance for doubtful accounts is a contra asset with a normal credit balance. It reduces the value of accounts receivable reported on the balance sheet. Companies should report accounts receivable at the net realizable value, accounts receivable minus allowance for doubtful accounts.

Companies often have a specific method of identifying the companies that it wants to include and the companies it wants to exclude. Thus, a $75 sale on credit to Mr. A raises the overall accounts receivable total in the general ledger by that amount while also increasing the balance listed for Mr. A in the subsidiary ledger. Either approach can be used as long as adequate support is generated for the numbers reported. However, financial accounting does stress the importance of consistency to help make the numbers comparable from year to year.

Contra Equity Account

In some cases, a customer whose account has been written off will subsequently pay part or all of his or her account. As this entry shows, the debit part of the entry is to the Allowance account. This net amount represents management’s estimate of the net realizable value of the firm’s receivables. Successful branding is why the Armani name signals style, exclusiveness, desirability.

This variance in treatment addresses taxpayers’ potential to manipulate when a bad debt is recognized. The allowance for doubtful accounts is a reduction of the total amount of accounts receivable appearing on a company’s balance sheet, and is listed as a deduction immediately below the accounts receivable line item. The allowance represents management’s best estimate of the amount of accounts receivable that will not be paid by customers.

Balance Sheet Aging of Receivables Method for Calculating Bad Debt Expenses

Now let’s say that a few weeks later, one of your customers tells you that they simply won’t be able to come up with $200 they owe you, and you want to write off their $200 account https://www.bookstime.com/articles/contra-asset-account receivable. Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts.

To protect your business, you can create an allowance for doubtful accounts. Like any other expense account, you can find your bad debt expenses in your general ledger. When you finally give up on collecting a debt (usually it’ll be in the form of a receivable account) and decide to remove it from your company’s accounts, you need to do so by recording an expense. It is sometimes referred to as the income statement approach because it focuses on the amount of bad debt expense recorded. If fewer accounts in dollars are written off than previously estimated, the Allowance account will have a credit balance prior to the adjustment.

Also note that it is a requirement that the estimation method be disclosed in the notes of financial statements so stakeholders can make informed decisions. At the end of an accounting period, the Allowance for Doubtful Accounts reduces the Accounts Receivable to produce Net Accounts Receivable. Note that allowance for doubtful accounts reduces the overall accounts receivable account, not a specific accounts receivable assigned to a customer. Because it is an estimation, it means the exact account that is (or will become) uncollectible is not yet known.